Why UK Accountants Are Still Confused On Pickups

Introduction

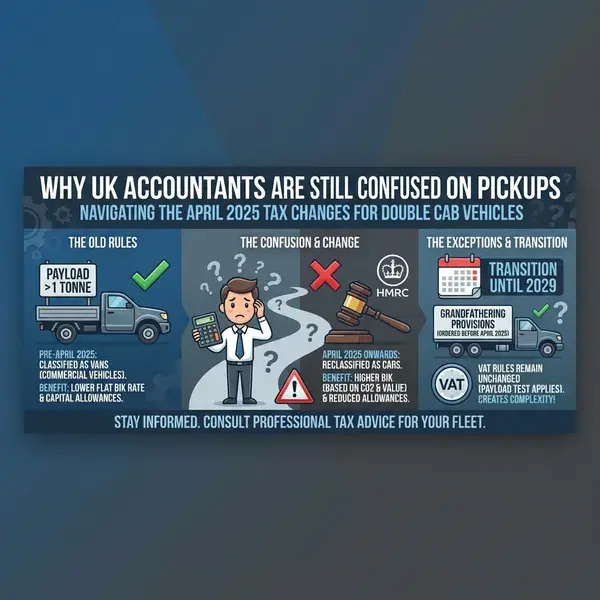

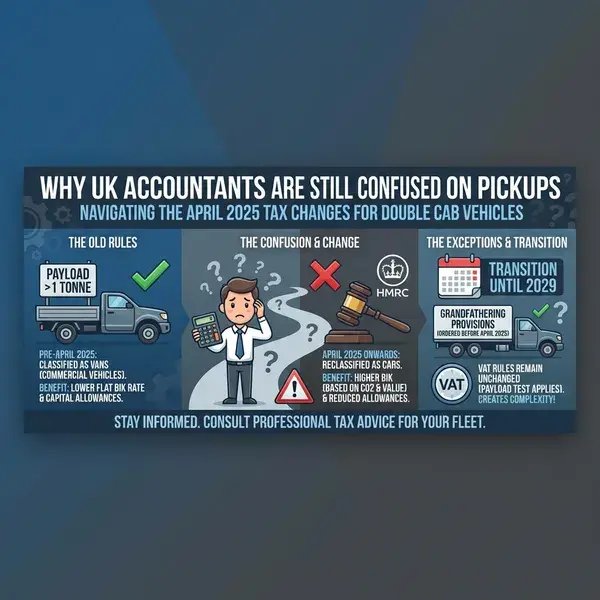

For years, company directors across the UK found a sweet spot in the tax code: the double-cab pickup. It looked and drove like an SUV but was treated as a van for tax. That meant generous VAT recovery and a low, flat Benefit-in-Kind (BIK) charge, regardless of price or CO₂.

But in April 2025, the government rewrote the rules. Suddenly, pickups are treated as cars for BIK and capital allowances (unless covered by transitional relief). Meanwhile, VAT rules didn’t change — they still hinge on whether the vehicle has a payload of at least 1,000 kg.

Pickup vs Car: The True Tax Cost (2025/26)

VAT Status

- ≥ 1,000kg payload: Not a car → VAT reclaim usually allowed.

- < 1,000kg payload: Car → VAT blocked (unless 100% business use).

BIK & Fuel

2025/26 rates:

- Van BIK: £4,020

- Van fuel benefit: £769

- Car fuel benefit multiplier: £28,200

- EV car BIK: 3%

Director’s Tax Bill

Basic Rate (20%)

Pickup as Van: £958

Pickup as Car: £4,392

EV Car: £270

This mismatch has left accountants scratching their heads and directors wondering:

-

Can I still reclaim VAT on a pickup?

-

Will my BIK bill rocket?

-

Does fuel allowance make any difference?

-

And what about EVs?

Let’s untangle the mess.

1. VAT: The 1,000kg Payload Test

1.1 The golden rule

For VAT, a car is any vehicle constructed mainly to carry passengers. But there’s an exception: vehicles with a payload of 1,000 kg or more are not cars.

-

≥1,000 kg payload → “Not a car” → VAT recovery generally allowed (subject to business use).

-

<1,000 kg payload → Treated as a car → VAT blocked unless 100% business use and unavailable for private use.

1.2 The hard-top trap

HMRC applies a standard 45 kg deduction for hard-tops on pickups. A model with a 1,020 kg payload can slip to 975 kg once fitted — flipping it from van to car for VAT.

1.3 Why directors care

If you’re VAT registered, reclaiming VAT on a £40,000+ pickup saves thousands. Lose that classification, and you carry the full VAT cost.

2. BIK: The April 2025 Change

2.1 The old world

-

Vans (including pickups): Flat BIK charge (2024/25: £3,960).

-

Cars: % of list price based on CO₂, up to 37%.

That’s why directors loved pickups. A £50k SUV could attract £15k+ of taxable benefit, while a pickup was stuck at ~£4k.

2.2 The new world (from April 2025)

-

Most double-cab pickups = cars for BIK.

-

Only those purchased, leased or ordered before 6 April 2025 keep the van treatment until 5 April 2029 (or until disposed of/lease ends).

2.3 Flat numbers for 2025/26

-

Van BIK: £4,020

-

Van fuel benefit: £769

-

Car fuel multiplier: £28,200

-

EV car BIK: 3%

3. Fuel Allowances

3.1 Cars

Fuel benefit = Car BIK % × £28,200.

Example: 30% BIK = £8,460 fuel benefit.

3.2 Vans

Flat £769 per year.

3.3 EVs

No fuel benefit on electricity. Company can pay for workplace or home charging without triggering a benefit.

4. Worked Examples

Case A: Director in a £45k pickup

-

As a van (grandfathered):

-

Van BIK = £4,020

-

Fuel = £769

-

Total = £4,789

-

-

As a car (30% BIK):

-

Car BIK = £13,500

-

Fuel = £8,460

-

Total = £21,960

-

Difference = £17,171 in taxable benefit.

Case B: EV company car (£45k)

-

BIK = 3% = £1,350

-

No fuel benefit

-

Total = £1,350

5. Director’s Tax Cost by Band

| Taxpayer | Pickup as Van | Pickup as Car | EV Car |

|---|---|---|---|

| Basic (20%) | £958 | £4,392 | £270 |

| Higher (40%) | £1,916 | £8,784 | £540 |

| Additional (45%) | £2,155 | £9,882 | £608 |

6. Infographic

7. FAQs

Q: Can I still reclaim VAT on a pickup in 2025?

Yes — as long as payload ≥1,000 kg. VAT rules didn’t change.

Q: Does ordering before April 2025 matter?

Yes — you can keep van BIK rules until April 2029 if you ordered/leased before 6 April 2025.

Q: Is fuel worth it?

Rarely for cars. For vans, maybe. For EVs, never an issue.

8. Final Takeaway

Pickups used to be the tax hack of choice. Today, they’re a minefield. The VAT and BIK rules no longer align:

-

VAT: Still based on 1,000 kg payload.

-

BIK: Now based on whether HMRC thinks it’s “car-like.”

-

EVs: Quietly becoming the cheapest company car option of all.

Moral of the story: Before signing that lease, check your payload, check your contract date, and check your accountant isn’t just as confused as everyone else